Missing a term insurance premium is a common concern for many policyholders in India. Life is unpredictable, and financial oversights or temporary cash flow issues can happen to anyone. However, because term insurance is a pure risk protection product, the consequences of non-payment are strictly governed by the Insurance Regulatory and Development Authority of India (IRDAI).

In this article, we will explore exactly What Happens If You Miss a Term Insurance Premium in India? and the steps you can take to ensure your family’s financial security remains intact.

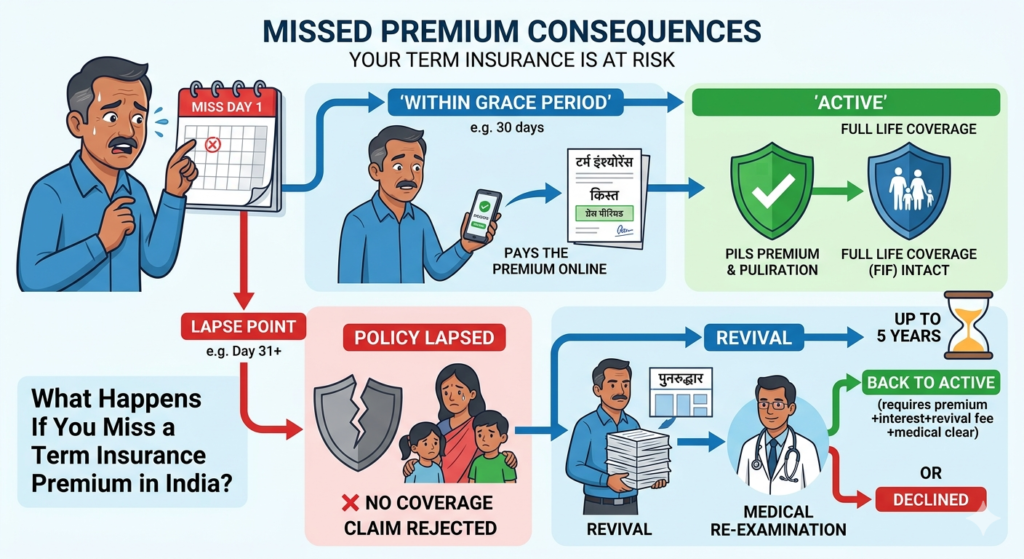

1. The Immediate Stage: The Grace Period

If you miss the due date, your policy does not disappear overnight. The IRDAI mandates a “Grace Period,” which is an extension granted to the policyholder to pay the premium without any loss of coverage.

- For Monthly Premium Modes: You generally get a grace period of 15 days.

- For Quarterly, Half-Yearly, or Yearly Modes: You get a grace period of 30 days.

During this time, your life cover remains active. If an unfortunate event occurs during the grace period, the insurer is legally bound to settle the claim, though they may deduct the outstanding premium amount from the final payout. This is the first and most critical window to address What Happens If You Miss a Term Insurance Premium in India?.

2. The Critical Stage: Policy Lapse

Once the grace period expires and the payment is still not made, the policy “lapses.” A lapsed policy means the contract between you and the insurance company is technically void.

Consequences of a Lapsed Policy:

- Zero Life Cover: If the policyholder passes away after the grace period ends, the nominee will receive no death benefit.

- Loss of Bonuses: Any loyalty additions or riders (like critical illness or accidental disability) attached to the policy will also cease to function.

- Loss of Tax Benefits: You can no longer claim tax deductions under Section 80C for a policy that is not active.

Understanding What Happens If You Miss a Term Insurance Premium in India? highlights that the primary risk isn’t just a fee; it is the total loss of the safety net you built for your family.

3. Comparison: Grace Period vs. Policy Lapse

To help you visualize the timeline, here is a breakdown of the status of your policy at different stages of non-payment.

| Feature | During Grace Period | After Grace Period (Lapse) |

| Life Cover Status | Active | Inactive / Void |

| Claim Settlement | Guaranteed (minus premium) | Rejected |

| Penalty/Interest | Usually None | Applicable (during revival) |

| Medical Check-up | Not Required | May be required for revival |

| Rider Benefits | Continued | Terminated |

4. The Recovery Stage: Policy Revival

If your policy has lapsed, you shouldn’t lose hope immediately. Most Indian insurers provide a “Revival Period,” typically spanning up to 5 years from the date of the first unpaid premium (depending on the specific product and IRDAI guidelines).

However, reviving a policy is more complex than simply paying a late fee. To answer What Happens If You Miss a Term Insurance Premium in India? in the context of revival, consider these requirements:

- Unpaid Premiums: You must pay all accumulated overdue premiums.

- Interest Charges: Insurers charge interest on the overdue amount, often ranging from 8% to 12% per annum.

- Evidence of Insurability: If the policy has been lapsed for a long time (usually more than 6 months), the insurer may ask for a “Declaration of Good Health” or even a fresh medical examination.

- Underwriting Risk: The insurer has the right to reject your revival request if your health status has significantly declined since you first bought the policy.

5. Why You Should Avoid Buying a New Policy Instead

Many people wonder, “If my policy lapses, why don’t I just buy a new one?” While this is an option, it is almost always more expensive.

When you buy a new term plan, your premium is calculated based on your current age. If you bought your original policy at age 30 and it lapses at age 37, a new policy will be significantly costlier because you are older. Additionally, any medical conditions developed during those seven years will further hike the premium or lead to an outright rejection. This is a vital part of knowing What Happens If You Miss a Term Insurance Premium in India?.

6. Proactive Measures to Prevent Non-Payment

To ensure you never have to deal with the stress of What Happens If You Miss a Term Insurance Premium in India?, follow these best practices:

- Set up NACH/ECS: Automate your payments through your bank account so the premium is deducted on the due date.

- Update Contact Details: Ensure your email and mobile number are current so you receive SMS and email reminders from the insurer.

- Opt for Annual Payments: Managing one payment a year is often easier than tracking twelve monthly ones, and it usually comes with a 30-day grace period instead of 15.

Summary

In conclusion, What Happens If You Miss a Term Insurance Premium in India? involves a transition from a safe grace period to a dangerous policy lapse. While the law allows for a revival window, the financial and health-related hurdles make it a difficult path. The best strategy is to treat your term insurance premium as a non-negotiable expense, ensuring your peace of mind and your family’s future are never at risk.

References for Further Reading:

- IRDAI Consumer Education Website

- Insurance Act, 1938 (Section 45)

- Life Insurance Corporation of India (LIC) Revival Guidelines

Also Read: Is Term Insurance Worth It in India

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Insurance products are complex; please consult with a certified advisor before making a final decision.