When you purchase or renew your vehicle insurance in 2026, the term “IDV” will be the most significant factor on your policy document. It is not just a random number; it is the cornerstone of your motor insurance contract.

In this article, we will simplify the concept and explain What is IDV in Vehicle Insurance? How to Calculate the Right Value for Your Car 2026 so you can ensure you are neither overpaying nor under-insured.

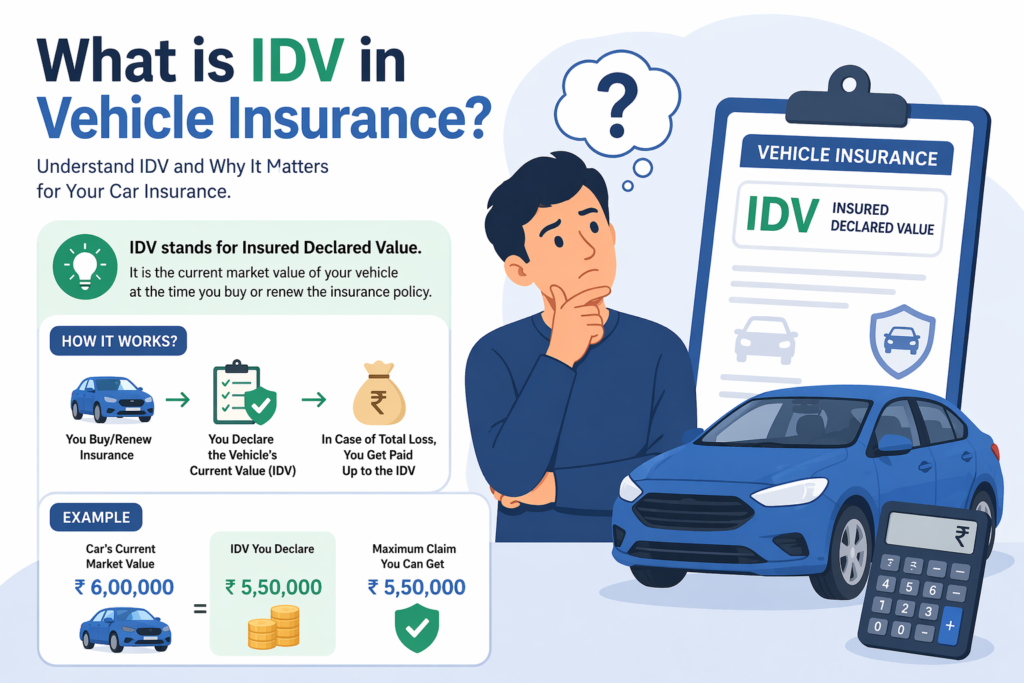

1. Defining IDV: The “Sum Insured” of Your Car

The Insured Declared Value (IDV) is the maximum amount your insurance provider is liable to pay you in the event of a “Total Loss” (when repair costs exceed 75% of the car’s value) or if the vehicle is stolen.

Think of it as the current market value of your vehicle. Unlike a life insurance policy where the sum insured remains constant, the IDV of a car decreases every year due to natural wear and tear. Understanding What is IDV in Vehicle Insurance? How to Calculate the Right Value for Your Car 2026 is essential because this value directly dictates the “Own Damage” (OD) component of your premium.

2. The Standard Formula for Calculation

The Insurance Regulatory and Development Authority of India (IRDAI) provides a uniform formula to ensure transparency across all insurers.

The Formula:

$$IDV = (\text{Manufacturer’s Listed Selling Price} – \text{Depreciation}) + (\text{Accessories} – \text{Depreciation on Accessories})$$

- Selling Price: This is the ex-showroom price, not the “on-road” price (which includes registration and road tax).

- Accessories: This includes non-factory fitted items like high-end music systems or specialized upholstery.

- Depreciation: This is the reduction in value based on the age of the vehicle.

3. The 2026 Depreciation Schedule

To accurately answer What is IDV in Vehicle Insurance? How to Calculate the Right Value for Your Car 2026, you must follow the IRDAI-mandated depreciation slabs. These percentages are applied to the ex-showroom price of the vehicle.

| Age of the Vehicle | Percentage of Depreciation |

| Up to 6 months | 5% |

| 6 months to 1 year | 15% |

| 1 year to 2 years | 20% |

| 2 years to 3 years | 30% |

| 3 years to 4 years | 40% |

| 4 years to 5 years | 50% |

| Beyond 5 years | Mutually Agreed/Negotiated |

For cars older than five years, the IDV is typically determined by a mutual agreement between the insurer and the policyholder, often based on the car’s condition and a valuation report from a certified surveyor.

4. The Impact of IDV on Your Premium

There is a direct, linear relationship between the IDV and the premium you pay.

- Higher IDV: Leads to a higher premium but ensures a larger payout in case of theft or total wreckage.

- Lower IDV: Reduces your annual premium but leaves you with a significant financial gap if you need to replace the vehicle.

When looking at What is IDV in Vehicle Insurance? How to Calculate the Right Value for Your Car 2026, many car owners make the mistake of choosing the lowest possible IDV to save money on the premium. This is risky because, in a total loss scenario, the insurer will only pay the declared value, which might be far below the actual market price of a replacement car.

5. Factors Influencing IDV in 2026

While age is the primary factor, several other variables can influence how you set the value:

- City of Registration: Ex-showroom prices vary slightly across Indian states due to local taxes.

- Make and Model: Luxury brands may have different negotiation terms for vehicles older than 5 years.

- Condition of the Vehicle: A well-maintained car with a full service history can sometimes command a slightly higher negotiated IDV in later years.

Knowing What is IDV in Vehicle Insurance? How to Calculate the Right Value for Your Car 2026 helps you negotiate with the insurance agent to find a “sweet spot” that offers fair protection without an exorbitant premium.

6. Common Myths About IDV

- “IDV is the Resale Value”: False. While they are related, resale value depends on market demand, whereas IDV is a fixed mathematical calculation for insurance purposes.

- “Registration and Insurance costs are included”: False. IDV only covers the cost of the vehicle and its accessories.

- “I can set any IDV I want”: False. You can usually only adjust it within a small range (typically +/- 5% to 10%) of the recommended value.

Summary

To conclude, What is IDV in Vehicle Insurance? How to Calculate the Right Value for Your Car 2026 is a question of balance. Your goal should be to declare a value that reflects the realistic cost of replacing your car today. Avoid the temptation of an ultra-low premium, as the “savings” will vanish the moment you face a major claim. Always check the current ex-showroom price of your specific car variant before renewing your policy to ensure the math is correct.

References for Further Reading:

- IRDAI – Motor Insurance Handbook

- General Insurance Council – Motor Insurance FAQ

- The Insurance Act, 1938

Also Read: What Happens If You Miss a Term Insurance Premium in India?

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Insurance products are complex; please consult with a certified advisor before making a final decision.