Choosing the right financial safety net is the most critical decision a breadwinner can make. In 2026, the Indian insurance landscape has evolved significantly with the introduction of Risk-Based Capital (RBC) frameworks and digital-first policies. However, the fundamental question remains: What type of life insurance is best for a family?

To answer this, we must look beyond marketing brochures and examine real claim settlement data, tax efficiency, and the “Human Life Value” (HLV) required to sustain a household in today’s economy.

The 2026 Comparison: Term, ULIP, and Endowment

When determining what type of life insurance is best for a family, you generally choose between three core structures. Each serves a different purpose based on your financial maturity and risk appetite.

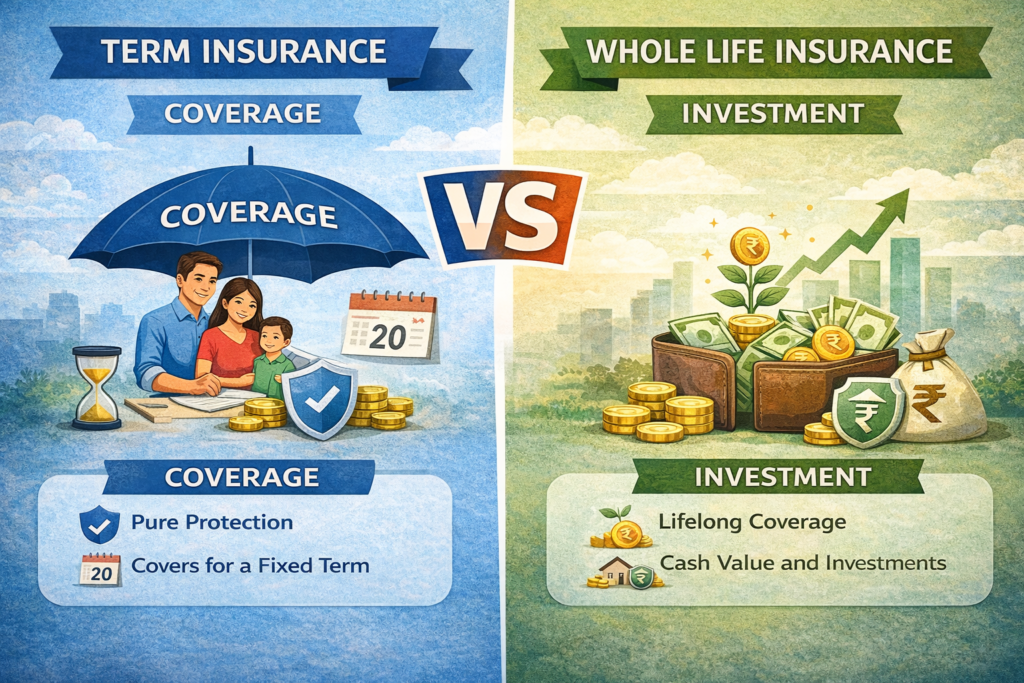

1. Pure Term Life Insurance

Term insurance is often cited by financial planners as the primary answer to what type of life insurance is best for a family. It offers a high sum assured for a very low premium. In 2026, a healthy 30-year-old male can secure a ₹1 Crore cover for approximately ₹700–₹900 per month.

- Best for: High-protection needs, income replacement, and covering large liabilities like home loans.

2. Unit Linked Insurance Plans (ULIPs)

Modern ULIPs in 2026 have become much more transparent. They allow you to invest in equity or debt markets while providing a life cover.

- Best for: Wealth creation with tax-free maturity (subject to premium caps).

3. Endowment and Savings Plans

These are traditional plans that offer “guaranteed” returns. While the life cover is usually lower (often 10x the annual premium), they provide a disciplined way to save for specific milestones.

- Best for: Extremely risk-averse individuals looking for a guaranteed corpus for a child’s education.

Comparative Data Table: Insurance Types at a Glance (2026)

| Feature | Term Insurance | ULIP | Endowment Plan |

| Primary Focus | Pure Protection | Wealth + Protection | Guaranteed Savings |

| Sum Assured | Very High (e.g., ₹2 Cr) | Moderate (10x Premium) | Low (10x Premium) |

| Maturity Benefit | Usually None* | Market-linked | Sum Assured + Bonus |

| Lock-in Period | None | 5 Years (IRDAI Mandate) | Policy Term |

| Avg. Yearly Premium | ₹10,000 – ₹20,000 | ₹50,000+ | ₹50,000+ |

*Note: Term with Return of Premium (TROP) is available but costs significantly more.

Key Metrics for Selection: Solvency and Settlement

When you ask what type of life insurance is best for a family, the answer must include the reliability of the provider. You should never buy a policy without checking these two IRDAI-mandated metrics:

1. Claim Settlement Ratio (CSR)

This indicates the percentage of claims the company paid out of the total claims received. For 2026, top-tier insurers like HDFC Life, Shriram Life, and Aditya Birla Sun Life have maintained CSRs above 99%.

- Reference: You can verify latest statistics on the IRDAI Annual Reports.

2. Solvency Ratio

This measures the insurer’s ability to pay out claims in a “worst-case scenario.” The IRDAI requires a minimum of 1.5 (150%). As of Q1 2026, many leading insurers are operating at 1.9 to 2.1, indicating strong financial health.

Tax Benefits and Regulations in 2026

Understanding the tax implications is vital when deciding what type of life insurance is best for a family.

- Section 80C: Premiums up to ₹1.5 Lakh remain deductible from taxable income under the old tax regime.

- Section 10(10D): The death benefit received by your family is 100% tax-free.

- Premium Caps: For ULIPs issued after February 2021, maturity is tax-free only if the total annual premium is below ₹2.5 Lakh. For non-linked plans (Endowment), the cap is ₹5 Lakh for policies issued after April 2023.

You can also read: What is TROP? Why it’s the ‘Money Back’ Term Plan you need.

The Verdict: How to Choose?

If you are the sole earner, the most logical answer to what type of life insurance is best for a family is a Pure Term Insurance Plan. It is the only product that ensures your family can maintain their standard of living, pay off a home loan, and fund a child’s university education for a premium that costs less than a weekend dinner.

The “Hybrid” Strategy: Many Indian families in 2026 follow the “15x Rule.”

- Buy a Term Plan with a sum assured equal to 15 times your annual income.

- Use the money “saved” from lower premiums to invest in a diversified Mutual Fund SIP or a low-cost ULIP for long-term growth.

Before finalizing, always use a Human Life Value (HLV) Calculator to ensure your cover isn’t just a number, but a calculated reality for your family’s future.

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Insurance products are complex; please consult with a certified advisor before making a final decision.