Term insurance is widely considered the most cost-effective way to secure a family’s financial future. However, one common psychological barrier for Indian buyers is the “lack of returns” if they outlive the policy. This is where Term Insurance with Return of Premium (TROP) comes into play, offering a middle ground between pure protection and money-back security.

In this article, we will break down the mechanics, costs, and benefits of Term Insurance with Return of Premium to help you decide if it is the right choice for your financial portfolio.

1. What is Term Insurance with Return of Premium?

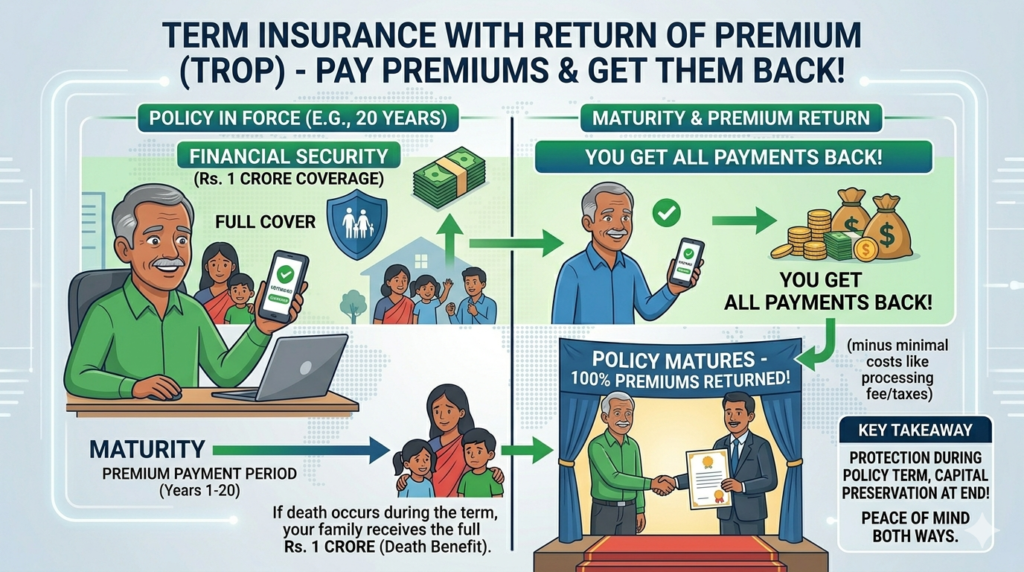

Unlike a standard term plan where the premiums are “lost” if the policyholder survives the term, Term Insurance with Return of Premium is a variant that acts as a savings-cum-protection tool. Under this plan, if the life assured survives the entire policy tenure, the insurance company refunds the total base premiums paid over the years.

It essentially functions as a zero-cost life cover in the long run, as the “cost” of the insurance is returned to you at maturity. This psychological comfort makes Term Insurance with Return of Premium one of the most popular products in the Indian insurance market today.

2. Key Features of TROP Plans

The Insurance Regulatory and Development Authority of India (IRDAI) ensures that these plans are transparent. Here are the defining features:

- Death Benefit: If the policyholder passes away during the term, the nominee receives the full Sum Assured.

- Maturity Benefit: If the policyholder survives the term, they receive a refund of the total premiums paid (excluding GST, rider premiums, and extra underwriting loadings).

- Surrender Value: Unlike pure term plans which usually have no exit value, Term Insurance with Return of Premium plans often acquire a surrender value after a specific period (usually 2 or 3 years of consistent premium payments).

- Tax Efficiency: Premiums are eligible for deduction under Section 80C, and the maturity amount is generally tax-free under Section 10(10D).

3. Comparison: Pure Term Insurance vs. TROP

Choosing between these two depends on your financial goals. Below is a factual comparison of how Term Insurance with Return of Premium stacks up against a standard term plan.

| Feature | Pure Term Insurance | Term Insurance with Return of Premium |

| Primary Objective | Pure Risk Protection | Protection + Premium Refund |

| Premium Cost | Low / Affordable | Higher (usually 1.5x to 2x more) |

| Survival Benefit | Nil | Refund of all base premiums |

| Surrender Value | Generally Nil | Paid after 2-3 years of premium |

| Ideal For | High cover at lowest cost | Those who want “money back” |

4. Understanding the Cost Factor

While the idea of getting your money back is appealing, it is important to note that Term Insurance with Return of Premium comes with a significantly higher price tag.

For instance, a 30-year-old non-smoker seeking a ₹1 Crore cover for 30 years might pay approximately ₹12,000 annually for a pure term plan. For a Term Insurance with Return of Premium version of the same policy, the premium could jump to ₹22,000 or more. The insurer uses the “extra” premium to invest and generate the corpus required to pay you back at the end of 30 years.

5. Tax Benefits and Regulatory Norms

In India, the tax treatment of Term Insurance with Return of Premium is a major highlight.

- Section 80C: You can claim a deduction of up to ₹1.5 lakh on the premiums paid annually (under the Old Tax Regime).

- Section 10(10D): The maturity amount received under Term Insurance with Return of Premium is exempt from tax, provided the annual premium does not exceed 10% of the sum assured.

- GST Impact: Currently, term insurance premiums attract 18% GST. It is important to remember that when the insurer returns your premium at maturity, the GST component is not refunded—only the base premium is.

6. Who Should Opt for TROP?

Term Insurance with Return of Premium is not a one-size-fits-all product. It is most suitable for:

- Risk-Averse Individuals: Those who feel uncomfortable paying for a service they might “never use” (i.e., if they don’t die during the term).

- Forced Savings Seekers: People who find it difficult to maintain a separate long-term investment discipline and prefer the “built-in” refund of an insurance policy.

- People with Surplus Cash Flow: If you can afford the higher premiums without compromising on the total Sum Assured you need, Term Insurance with Return of Premium provides a guaranteed return of capital.

Conclusion

Deciding on Term Insurance with Return of Premium requires balancing the desire for “money back” against the higher cost of the premium. While it is more expensive than pure term insurance, the guaranteed maturity benefit and surrender value provide a layer of financial flexibility that pure term plans lack. Always compare the Internal Rate of Return (IRR) of a TROP plan against buying a pure term plan and investing the difference in other instruments like PPF or Mutual Funds before making your final decision.

References for Further Reading:

- IRDAI Official Portal – Policyholder Education

- Income Tax Department – Section 80C and 10(10D) Explained

- Life Insurance Council of India – Types of Plans

Also Read: What Happens If You Miss a Term Insurance Premium in India

Also Read: Best Term Insurance Plans for Self-Employed in India

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Insurance products are complex; please consult with a certified advisor before making a final decision.