As India’s automotive landscape shifts toward green mobility in 2026, many car buyers are left wondering how the transition affects their recurring costs. While fuel savings are obvious, the insurance math is slightly more complex.

In this article, we compare EV vs. Petrol Car Insurance and explain why your coverage needs might change when you ditch the combustion engine for a battery.

1. The Regulatory Edge: IRDAI Discounts

To encourage the adoption of eco-friendly vehicles, the Insurance Regulatory and Development Authority of India (IRDAI) currently offers a significant incentive for electric vehicle owners.

For the mandatory Third-Party (TP) insurance component, EV owners receive a 15% discount compared to the rates for similar petrol or diesel vehicles. This is a direct statutory benefit of choosing EV vs. Petrol Car Insurance. While the TP rates for petrol cars are determined by cubic capacity (cc), EV rates are based on the motor’s power output in kilowatts (kW).

2. Own Damage (OD) Premiums: The Reality of 2026

While you save on Third-Party rates, the “Own Damage” portion of your premium—which covers theft, accidents, and natural disasters—is often 20% to 25% higher for EVs than for petrol cars.

This price gap in EV vs. Petrol Car Insurance exists because:

- High Component Costs: The battery pack typically accounts for 40% to 60% of an EV’s value.

- Specialized Labor: Repairing an EV requires high-voltage certified technicians and specialized diagnostic tools, which increases labor costs.

- Total Loss Risk: Even minor underbody impacts can compromise the battery casing. In many cases, insurers prefer to declare a “Total Loss” rather than risk a battery fire, leading to higher risk pricing.

3. Comparison: Premium Breakdown (Estimated 2026)

Below is a factual comparison between a standard Petrol SUV and its EV counterpart in the Indian market.

| Feature | Petrol SUV (e.g., 1.2L Engine) | Electric SUV (e.g., 30-65 kW) |

| Third-Party Premium | Higher (Standard Rate) | 15% Discounted Rate |

| Own Damage Premium | Moderate | High (approx. 20% more) |

| Required Add-ons | Standard (Engine Protect) | Critical (Battery Protect) |

| IDV Depreciation | Standard (Schedule-based) | High (due to tech obsolescence) |

| Maintenance Link | High (Moving parts) | Low (Simple drivetrain) |

4. Critical Add-Ons for EVs

When navigating EV vs. Petrol Car Insurance, the “Add-ons” you choose are just as important as the base policy. For a petrol car, you might prioritize “Engine Protector.” For an EV, you must look for:

- Battery Protection Cover: Standard policies may not cover gradual battery degradation or damage caused by a short circuit or water ingress.

- Smart Charger Cover: Your home charging station is a high-value asset. Ensuring your insurance covers the charger and its wiring against power surges or theft is vital.

- Zero Depreciation: Given that EV parts are 30% more expensive to replace, “Zero Dep” is almost mandatory to avoid massive out-of-pocket expenses during a claim.

5. Technology and Telematics in 2026

A unique feature of the 2026 insurance market is the rise of Usage-Based Insurance (UBI). Because EVs are highly connected, insurers can offer “Pay-How-You-Drive” (PHYD) plans.

Safe driving habits—like smooth braking and steady acceleration—are easier to track in an EV. This allows EV owners to potentially offset their higher OD premiums with “Safe Driver” discounts of up to 10% to 25%. This is a modern evolution in the EV vs. Petrol Car Insurance debate that rewards tech-savvy, cautious drivers.

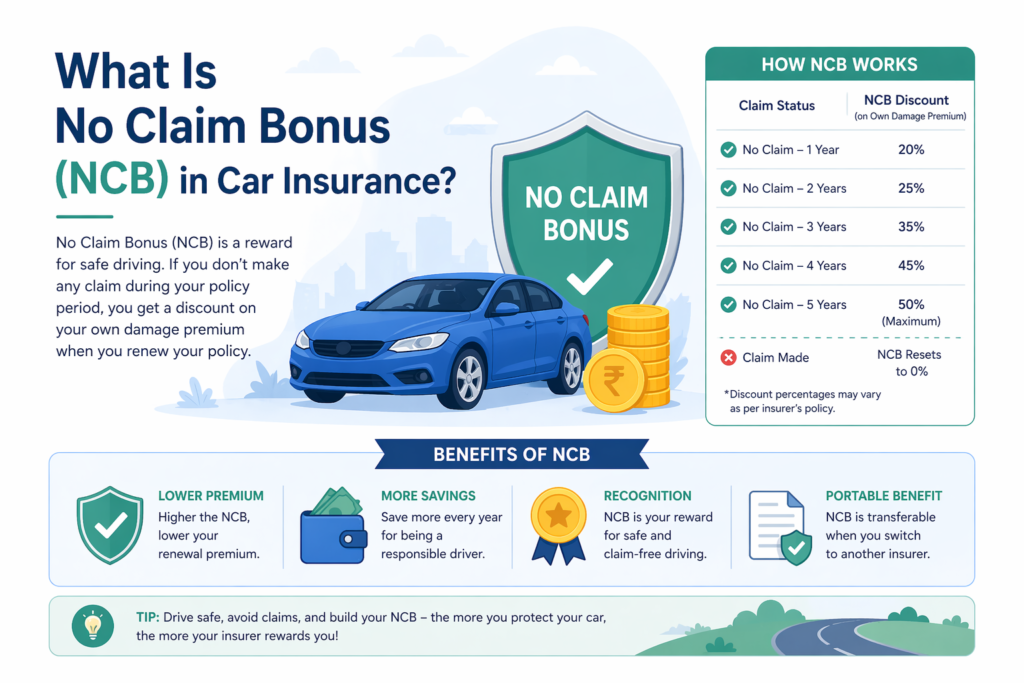

Do give it a read: What Is No Claim Bonus (NCB) in Car Insurance

6. Resale and IDV Considerations

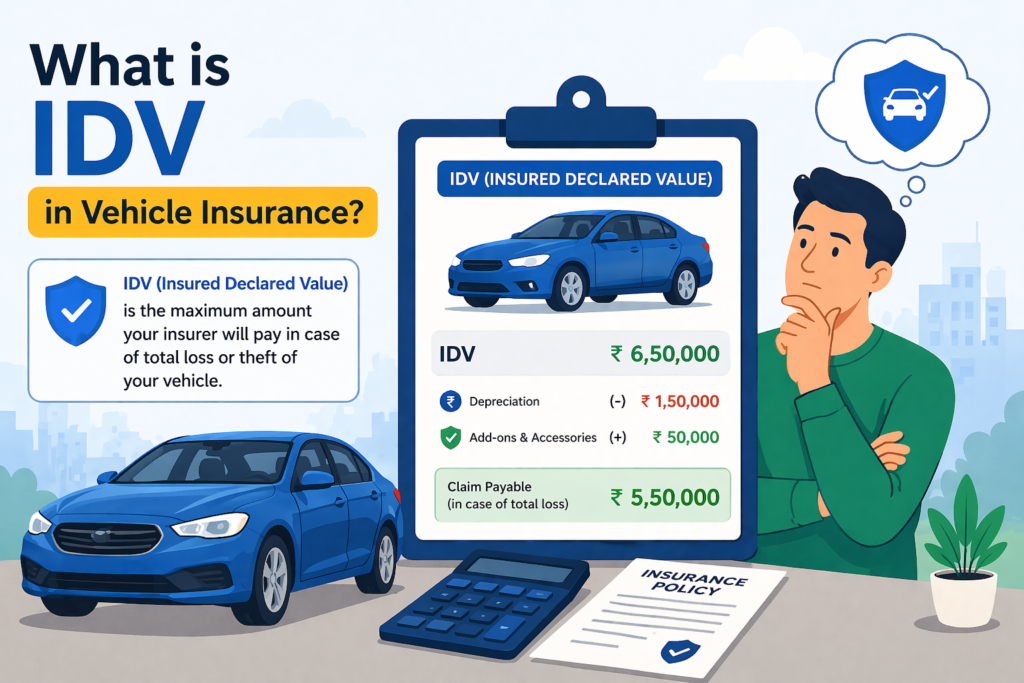

The Insured Declared Value (IDV) of an EV often drops faster than that of a petrol car. This is because battery technology is evolving rapidly, making older models less desirable. When setting your IDV, ensure it reflects the true replacement cost of the battery, as a low IDV can lead to a massive financial loss if the vehicle is stolen or totaled.

Conclusion

The choice between EV vs. Petrol Car Insurance isn’t just about finding the cheapest quote; it’s about protecting a high-tech investment. While you enjoy IRDAI-mandated discounts on third-party cover and lower running costs, you must be prepared for higher upfront premiums for comprehensive protection. Investing in a robust “Battery Protect” add-on and leveraging telematics discounts are the smartest ways to manage your insurance budget in 2026.

Do Read: What is IDV in Vehicle Insurance? How to Calculate the Right Value for Your Car 2026

References for Further Reading:

- IRDAI Notification on EV Third-Party Rates

- Policybazaar – Guide to Electric Vehicle Insurance

- The Insurance Act, 1938 (Section 64VB)

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Insurance products are complex; please consult with a certified advisor before making a final decision.