Entering the world of financial planning can feel like navigating a maze, especially when confronted with complex jargon and endless policy options. However, mastering insurance tips for beginners is one of the most impactful steps you can take to protect your future. In 2026, insurance is no longer just about “buying a policy”—it is about building a customized safety net that evolves with your life stages.

Whether you are a fresh graduate starting your first job or a young couple planning a family, this guide provides actionable, fact-based insurance tips for beginners to help you make informed decisions without the stress.

1. Why Insurance Matters More Than Ever in 2026

Before diving into specific insurance tips for beginners, it is essential to understand the “why.” In an era of rising medical inflation—which in India is currently hovering around 14–15%—a single emergency can wipe out years of disciplined savings. Insurance acts as a shock absorber for your finances, ensuring that unexpected events like illness, accidents, or the loss of a breadwinner do not lead to a debt trap.

The Core Philosophy: Protection First

Many beginners make the mistake of looking at insurance as an investment or a tax-saving tool. One of the most vital insurance tips for beginners is to separate “Protection” from “Investment.” Your primary goal should be to cover risk; growing your wealth should happen through other instruments like Mutual Funds or PPF.

2. Term Insurance: The Non-Negotiable First Step

If you have anyone financially dependent on you (parents, spouse, or children), Term Insurance is your highest priority. It is the purest and most affordable form of life insurance.

- How it Works: You pay a small premium for a large “Sum Assured.” If you pass away during the policy term, your family receives the money.

- The 20x Rule: A standard recommendation among insurance tips for beginners is to ensure your life cover is at least 20 times your annual income.

- Start Early: In 2026, a 25-year-old can lock in a ₹1 Crore cover for as little as ₹800–₹1,000 per month. If you wait until age 40, that same cover could cost three times more.

3. Health Insurance: Navigating the Rising Cost of Care

Medical emergencies are the leading cause of bankruptcy for middle-class families. When researching insurance tips for beginners, you will find that a basic corporate health plan is rarely enough.

Read our guide on: Best Insurance for Middle Class Families

Why Your Corporate Policy Isn’t Sufficient

Most employers provide a base cover of ₹3 Lakh to ₹5 Lakh. While this sounds like a lot, a major surgery or a prolonged ICU stay in a Tier-1 city can easily exceed ₹10 Lakh.

- Buy a Private Plan: Always maintain a personal health policy independent of your job. If you switch careers or face a layoff, your personal policy stays active.

- Look for “Restore” Benefits: This is a top-tier feature in 2026. If you exhaust your limit for one illness, the company “restores” it for the next one within the same year.

- Check Room Rent Caps: Ensure your policy does not have a “1% of Sum Insured” room rent cap, as this leads to massive out-of-pocket expenses during discharge.

4. Understanding Key Insurance Metrics

One of the most technical insurance tips for beginners involves looking at the data behind the company. Never pick an insurer based on a celebrity ad; look at these two numbers instead:

A. Claim Settlement Ratio (CSR)

This is the percentage of claims the company has paid out of the total claims received. In 2026, you should prioritize insurers with a CSR of 98% or higher. This data is publicly available in the IRDAI (Insurance Regulatory and Development Authority of India) annual reports.

B. Solvency Ratio

The Solvency Ratio indicates whether the company has enough “extra” cash to pay claims in a massive disaster. The IRDAI mandate is a minimum of 1.5 (150%). A company with a ratio of 1.8 to 2.1 is considered very stable.

| Metric | Target for Beginners | Why it Matters |

| CSR | > 98% | Probability of your claim being paid |

| Solvency Ratio | > 1.5 | Financial strength of the insurer |

| Network Hospitals | > 10,000 | Ease of cashless treatment |

5. The “Hidden” Pillars: Personal Accident & Critical Illness

A comprehensive strategy for insurance tips for beginners must go beyond just “Death” and “Hospitalization.” You must also insure your ability to earn.

- Personal Accident Insurance: If an accident leads to a “Permanent Total Disability” (like losing mobility), you may survive but lose your ability to work. This policy provides a lump sum to help modify your home or sustain your lifestyle.

- Critical Illness Cover: Standard health insurance pays the hospital bill. A Critical Illness plan pays you a lump sum upon the diagnosis of severe diseases like Cancer or Kidney Failure. This money can be used for experimental treatments or to pay off your home loan while you recover.

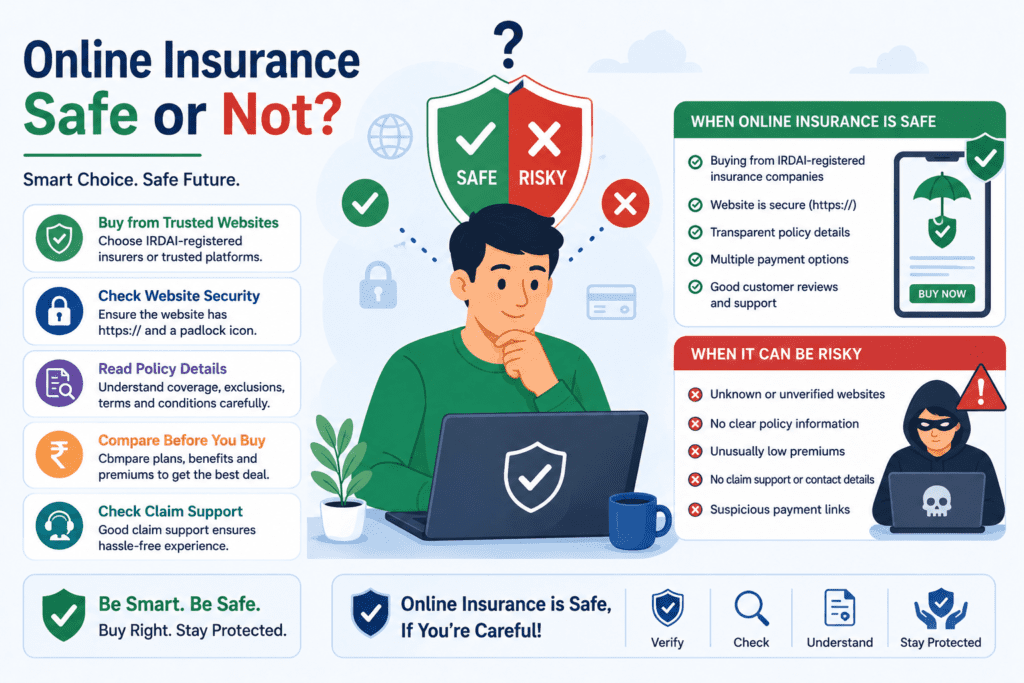

6. How to Buy: Online vs. Offline

In 2026, digital platforms have revolutionized the industry. One of the best insurance tips for beginners is to compare and buy online.

- Transparency: Online portals allow you to see the “Policy Wording” directly.

- Lower Cost: Because there is no middleman or agent commission, online policies are often 10–20% cheaper.

- Honesty is Key: When filling out your digital form, never hide a smoking habit or a pre-existing disease. In 2026, insurers use AI and medical data integration; a small lie today will lead to a rejected claim for your family later.

7. Tax Benefits: The Added Perk

While protection is the goal, the tax benefits are a welcome bonus. For those looking for insurance tips for beginners regarding taxes:

- Section 80C: Life insurance premiums (up to ₹1.5 Lakh) are deductible under the old tax regime.

- Section 80D: Health insurance premiums provide a deduction of up to ₹25,000 for yourself and an additional ₹25,000–₹50,000 for your parents.

- Section 10(10D): The death benefit received by your family is entirely tax-free.

8. Summary Checklist for Every Beginner

To wrap up these insurance tips for beginners, here is your 2026 roadmap:

- Term Plan: Get a cover that is 20x your annual salary.

- Health Plan: Get at least ₹10 Lakhs of personal family floater cover.

- Accident Plan: Secure a policy that covers Permanent Disability.

- Critical Illness: Add a rider to your health or term plan.

- Review Yearly: As your salary increases or you get married, update your cover amounts.

You can also check our guide in hindi: Health Insurance Claim Reject Kyun Hota Hai?

9. Common Mistakes to Avoid

No list of insurance tips for beginners is complete without warnings:

- Don’t “Buy and Forget”: An insurance policy is a living document. Review it every time you have a major life event (marriage, birth of a child, home loan).

- Avoid “Money-Back” Policies: These often provide a 4–5% return, which barely beats inflation, and the life cover they provide is usually insufficient for a middle-class family.

- Read the Exclusions: Know what is not covered. For example, most health plans don’t cover cosmetic surgeries or injuries sustained while under the influence of alcohol.

10. Conclusion

Mastering insurance tips for beginners is the ultimate act of love for your family. It ensures that no matter what life throws at you, your financial goals—your children’s education, your spouse’s security, and your home—remain protected. In 2026, the tools to be your own financial advocate are at your fingertips. Start small, stay honest in your applications, and build your shield one policy at a time.

How to File a Health Insurance Claim Online in India

Reference Links for Genuine Information:

- IRDAI (Insurance Regulatory and Development Authority of India): https://irdai.gov.in/

- Life Insurance Council of India: https://www.lifeinsurancecouncil.org/

- National Health Authority (PMJAY/Health Data): https://nha.gov.in/

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Insurance products are complex; please consult with a certified advisor before making a final decision.