For a middle-class family in India, financial planning is a delicate balancing act between current lifestyle needs and future aspirations. With medical inflation rising and the cost of education soaring in 2026, choosing the best insurance for middle class families is no longer just an option—it is a foundational necessity for wealth preservation.

A single hospital stay or the sudden loss of a breadwinner can derail years of savings. Therefore, a robust insurance portfolio must be built on three pillars: Protection, Health, and Liability.

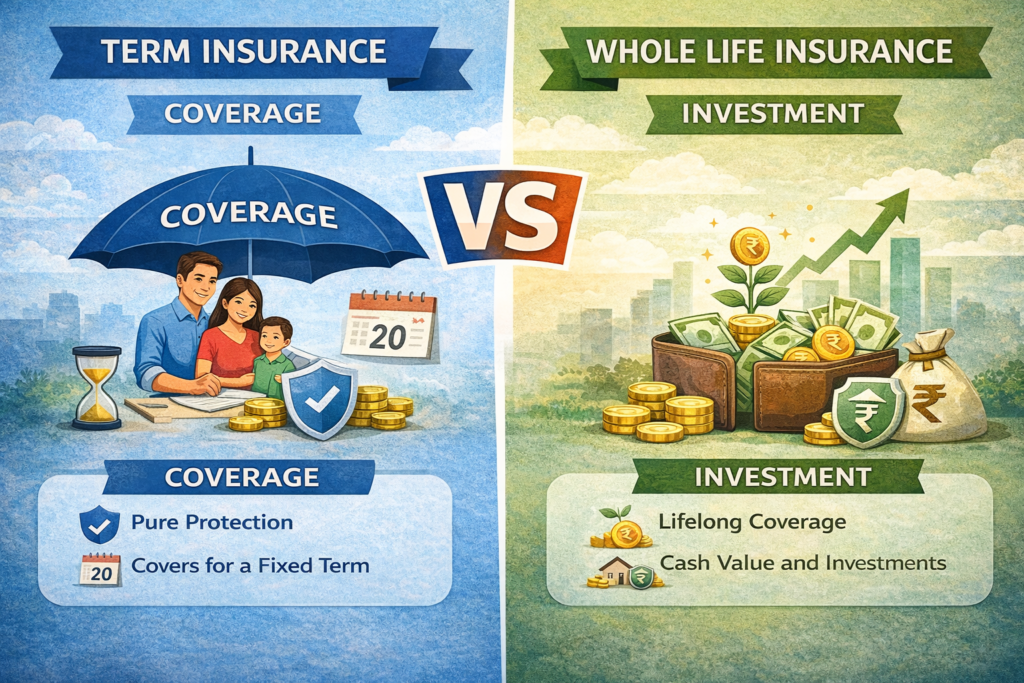

1. Term Insurance: The Foundation of Family Protection

When discussing the best insurance for middle class families, Term Insurance always takes the top spot. It is the purest form of life insurance, designed to replace the income of the breadwinner.

- High Sum Assured: Middle-class families often have liabilities like home loans or car EMIs. Term insurance provides a massive payout (e.g., ₹1 Crore or more) for a very small monthly premium.

- Income Replacement: The payout ensures that the spouse can maintain the household and children can continue their education without financial interruption.

- Cost-Effectiveness: In 2026, a 30-year-old can secure a ₹1 Crore cover for as low as ₹1,000–₹1,200 per month, making it accessible for every budget.

2. Health Insurance: Combatting Medical Inflation

Medical costs in India are rising at approximately 14–15% annually. For a middle-class household, a “Family Floater” plan is often cited as the best insurance for middle class families because it covers the spouse, children, and sometimes parents under a single umbrella.

- Cashless Hospitalization: Top insurers now have networks of over 10,000+ hospitals, ensuring you don’t have to arrange for cash during emergencies.

- Comprehensive Coverage: Look for plans that include pre-and-post hospitalization, day-care procedures, and organ donor expenses.

- Restore Benefits: If one family member exhausts the limit, many modern plans “restore” the sum insured for the next illness, which is a vital feature for families.

Health Insurance Claim Reject Kyun Hota Hai?

3. Comparison of Insurance Needs for Middle-Class Families

The following table outlines the essential components required to build the best insurance for middle class families portfolio.

| Insurance Type | Recommended Cover | Why it’s Essential | 2026 Trend |

| Term Insurance | 15x–20x Annual Income | Income replacement & debt clearing | Digital-only plans with lower premiums |

| Family Floater Health | ₹10 Lakhs – ₹25 Lakhs | Protection against rising hospital bills | Inclusion of mental health and OPD |

| Personal Accident | ₹25 Lakhs – ₹50 Lakhs | Covers disability & loss of income | Global coverage riders |

| Critical Illness | ₹10 Lakhs (Lump Sum) | Covers Cancer, Stroke, Heart Attack | Accelerated payouts upon diagnosis |

4. The “15-15-15” Rule for Insurance Planning

To determine the best insurance for middle class families, many financial advisors in 2026 recommend the “15 Rule”:

- Life Cover: Should be at least 15 times your annual salary.

- Health Cover: Should cover at least 15% of your total liquid net worth or a minimum of ₹10 Lakhs.

- Critical Illness: Should be at least 1.5 times your annual income to cover lifestyle changes and recovery.

5. Critical Illness & Personal Accident: The Missing Pieces

Many people stop at life and health insurance, but the best insurance for middle class families should also include disability and trauma protection.

- Critical Illness Rider: Standard health insurance pays the hospital bill. A Critical Illness plan pays you a lump sum upon diagnosis of diseases like cancer or kidney failure. This money can be used for debt repayment or specialized treatment not covered by standard plans.

- Personal Accident Cover: While life insurance pays on death, an accident plan pays for Permanent Total Disability (PTD). If a breadwinner survives an accident but cannot work, this policy provides the financial support needed for home modifications and daily expenses.

6. Regulatory Safety and Tax Benefits

In 2026, the IRDAI (Insurance Regulatory and Development Authority of India) has made the insurance sector extremely transparent. For a middle-class family, these protections ensure that the best insurance for middle class families is also the most reliable.

- Claim Settlement Ratio (CSR): Always choose an insurer with a CSR above 98%. This data is publicly available in the IRDAI annual reports.

- Tax Savings: Premiums paid for life insurance are deductible under Section 80C (up to ₹1.5 Lakh), and health insurance premiums are deductible under Section 80D (up to ₹25,000 for self/family and an additional amount for parents).

- 10(10D) Exemption: The death benefit received from a term plan is entirely tax-free for the nominee.

7. How to Choose the Best Insurance for Middle Class Families

If you are currently evaluating your options, follow this 3-step checklist:

- Check the Solvency Ratio: This indicates the insurer’s ability to pay out claims in a disaster. Look for a ratio above 1.5.

- Evaluate Sub-limits: Ensure your health insurance doesn’t have “Room Rent caps” that force you to pay out of pocket for a private room.

- Avoid Bundle Products: Often, “Endowment” or “Money-back” plans provide low returns and low cover. For the best insurance for middle class families, it is usually better to buy a pure Term Plan and invest the remaining money in PPF or Mutual Funds.

Must read guide on: Which is Better Term or Life Insurance?

Conclusion

The best insurance for middle class families is not a single product but a strategy. By combining a high-cover Term Plan, a comprehensive Family Floater Health Plan, and a Critical Illness rider, you create a 360-degree shield around your family’s future. In 2026, the ease of digital renewals and AI-driven claim settlements makes it easier than ever to stay protected.

Don’t wait for a crisis to realize the value of a safety net. Start with a basic term and health plan today and upgrade as your income grows.

Reference Links for Genuine Information:

- IRDAI (Insurance Regulatory and Development Authority of India): https://irdai.gov.in/

- Life Insurance Council of India: https://www.lifeinsurancecouncil.org/

- National Health Authority (PMJAY/Health Insurance Info): https://nha.gov.in/

Read our detailed guide on: How to File a Health Insurance Claim Online in India

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Insurance products are complex; please consult with a certified advisor before making a final decision.