Deciding how to protect your family’s financial future is one of the most significant responsibilities of a breadwinner. In the Indian financial landscape of 2026, the debate over which is better term or life insurance (specifically permanent or endowment-style life insurance) remains a top priority for households. While both products offer a safety net, they serve very different financial philosophies.

In this guide, we will break down the mechanics, costs, and strategic value of both options to help you determine which is better term or life insurance for your specific needs.

1. Understanding the Core Difference

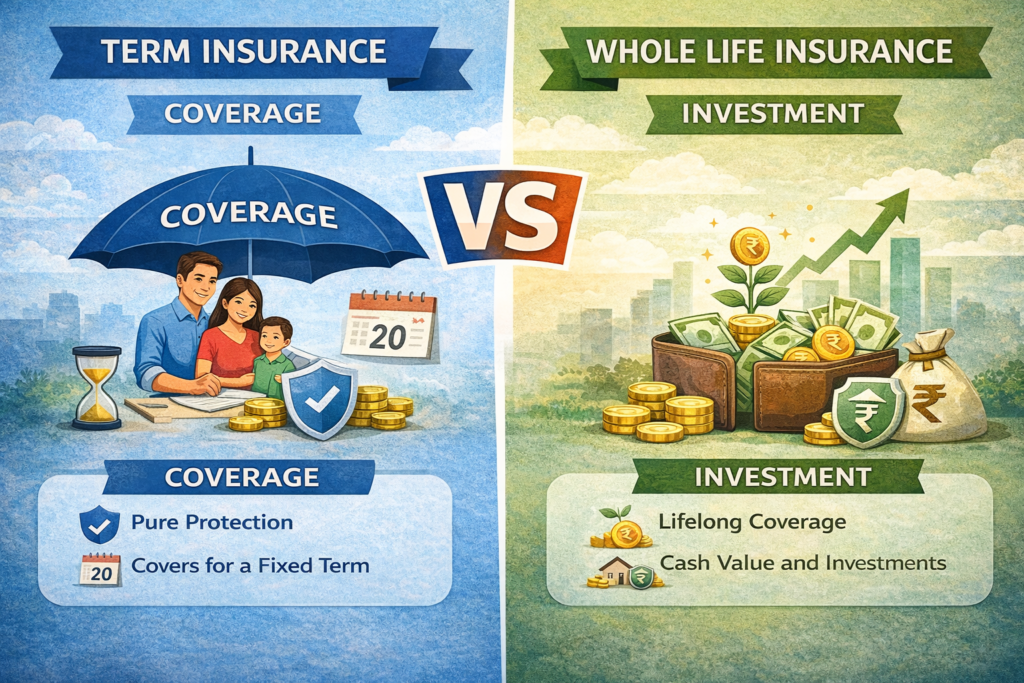

To evaluate which is better term or life insurance, one must first understand that “Life Insurance” is an umbrella term. In common Indian parlance, “Life Insurance” usually refers to traditional policies like Endowment or Money-Back plans that combine insurance with savings. Term Insurance, on the other hand, is pure protection.

Term Insurance (Pure Protection)

Term insurance provides coverage for a specific period (the “term”). If the policyholder passes away during this time, the nominee receives the sum assured. If the policyholder survives the term, there is typically no maturity benefit. This simplicity is why it remains a strong contender when debating which is better term or life insurance.

Traditional Life Insurance (Savings + Protection)

Traditional life insurance plans, such as Endowment policies, cover you for a longer duration and include a “savings” component. A portion of your premium goes toward life cover, while the rest is invested by the insurer to provide a maturity benefit (bonus) at the end of the policy term.

2. Cost vs. Coverage: The Reality Check

The most striking difference when asking which is better term or life insurance is the premium-to-cover ratio.

In 2026, a 30-year-old non-smoker can often secure a ₹1 Crore Term Insurance cover for approximately ₹10,000 to ₹15,000 per year. In contrast, to get the same ₹1 Crore cover through a traditional Endowment plan, the annual premium could exceed ₹8 Lakhs to ₹10 Lakhs. Because the premium for traditional plans is so high, most people end up “under-insured,” choosing a smaller cover (like ₹5 Lakhs or ₹10 Lakhs) just to keep the premium affordable.

3. Comparative Analysis: Term vs. Traditional Life Insurance

The following table provides a factual breakdown to help you visualize which is better term or life insurance based on various financial parameters.

| Feature | Term Insurance | Traditional Life Insurance (Endowment) |

| Primary Goal | High Risk Protection | Disciplined Savings + Protection |

| Sum Assured | High (e.g., ₹1 Cr – ₹5 Cr) | Low (Usually 10x of annual premium) |

| Maturity Benefit | None (unless TROP is chosen) | Guaranteed Sum + Accrued Bonuses |

| Premium Cost | Very Low | Very High |

| Surrender Value | Generally Nil | Available after 2-3 years |

| Flexibility | High (Easy to exit/change) | Low (Heavy penalties for early exit) |

You can also read our guide on: Term Insurance vs Life Insurance in India: Key Differences Explained (2026)

4. The Wealth Creation Perspective

When investors analyze which is better term or life insurance, they often look at the “Opportunity Cost.”

If you choose a Term Plan and invest the difference (the money you saved by not buying an expensive Endowment plan) into a diversified portfolio of Mutual Funds or Public Provident Fund (PPF), your total wealth at the end of 20 years is statistically likely to be significantly higher than the maturity benefit of a traditional life insurance policy.

Traditional plans in India typically offer internal rates of return (IRR) ranging from 4% to 6%. In an economy where inflation is a constant factor, this may not be enough to maintain purchasing power. Therefore, for those focused on aggressive wealth growth, the answer to which is better term or life insurance often leans toward the Term Insurance + Separate Investment strategy.

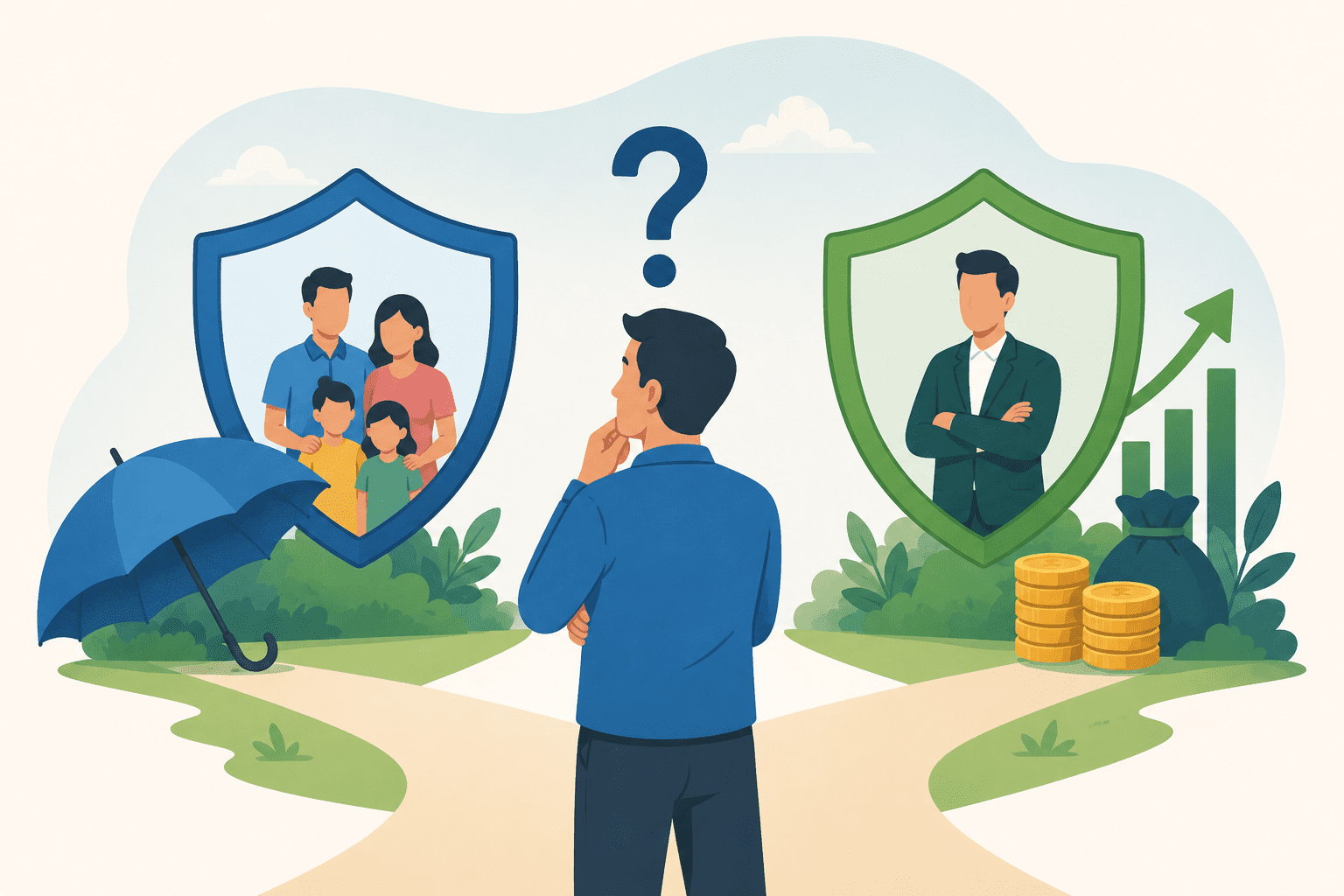

5. Who Should Choose Which?

The answer to which is better term or life insurance is not universal; it depends on your behavioral finance traits.

- Choose Term Insurance if: You are the primary breadwinner, you have liabilities (loans), and you want the maximum possible protection for your family at the lowest cost. It is ideal for those who have the discipline to invest their savings separately.

- Choose Traditional Life Insurance if: You are extremely risk-averse and struggle with disciplined savings. These plans act as a “forced savings” mechanism where the fear of losing the policy keeps you paying the premium, ensuring a lump sum is available for future milestones like a child’s wedding.

6. Regulatory Safety and Tax Benefits (2026)

In 2026, both products are strictly regulated by the IRDAI (Insurance Regulatory and Development Authority of India), ensuring high claim settlement standards.

- Tax Savings: Both plans offer deductions under Section 80C (up to ₹1.5 Lakh) in the old tax regime.

- Tax-Free Payouts: Under Section 10(10D), the death benefit for both is tax-free. However, for traditional plans, maturity is only tax-free if the annual premium is less than ₹5 Lakhs (for policies issued after April 2023).

Best Age to Buy Life Insurance in India (2026 Guide)

7. The Verdict

When strictly evaluating which is better term or life insurance for family protection, Term Insurance is the winner. It fulfills the primary purpose of insurance—risk cover—without diluting it with low-return investments. However, a small traditional policy can serve as a “safe” secondary layer for conservative investors.

Always check the Claim Settlement Ratio (CSR) of your insurer before buying. In 2026, look for companies with a CSR above 98% to ensure your family’s claims are handled reliably.

Online vs Offline Insurance in India: Which is Better in 2026

Reference Links

- IRDAI – Consumer Education Portal

- Life Insurance Council of India – Statistics and Forms

- Income Tax Department – Deductions under Section 80C

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Insurance products are complex; please consult with a certified advisor before making a final decision.