Understanding the car insurance claim process in India is essential for every car owner, especially if you have recently purchased a new vehicle. Many people buy insurance but are unsure what to do when an accident or damage occurs. Knowing the car insurance claim process in India in advance can save time, reduce stress, and help you get your claim settled smoothly.

In this guide, we will explain the car insurance claim process in India step by step, along with important tips and common mistakes to avoid.

Types of Car Insurance Claims in India

Before understanding the car insurance claim process in India, it’s important to know the two main types of claims:

1. Cashless Claim

In a cashless claim:

- Repairs are done at a network garage

- The insurer directly pays the garage

- You only pay for non-covered expenses

This is the most convenient option.

2. Reimbursement Claim

In a reimbursement claim:

- You pay for repairs first

- Submit bills and documents

- Insurance company reimburses the amount later

Useful when you use a non-network garage.

Step-by-Step Car Insurance Claim Process in India

Here is the complete car insurance claim process in India:

Step 1: Inform Your Insurance Company

As soon as an accident or damage occurs:

- Inform your insurer immediately

- Most companies have a 24/7 helpline

Delays in reporting may lead to claim rejection.

Step 2: File an FIR (if required)

An FIR (First Information Report) is required in cases like:

- Theft

- Major accidents

- Third-party damage

Always check with your insurer.

Step 3: Submit Required Documents

You’ll need:

- Policy document

- Driving license

- RC (Registration Certificate)

- FIR (if applicable)

- Claim form

Accurate documentation is crucial in the car insurance claim process in India.

Step 4: Inspection by Surveyor

The insurance company will assign a surveyor to:

- Inspect the damage

- Estimate repair cost

Do not start repairs before inspection unless approved.

Step 5: Repair the Vehicle

- For cashless → take your car to a network garage

- For reimbursement → choose any garage

Step 6: Claim Settlement

- Cashless → insurer pays garage directly

- Reimbursement → you get money after submission

This completes the car insurance claim process in India.

Important Documents Required

To ensure a smooth car insurance claim process in India, keep these ready:

- Insurance policy copy

- Driving license

- Vehicle registration certificate

- Repair bills and receipts

- Claim form

Common Mistakes to Avoid

When following the car insurance claim process in India, avoid:

- Delaying claim intimation

- Starting repairs before inspection

- Submitting incomplete documents

- Making small claims unnecessarily

These mistakes can delay or even reject your claim.

How Long Does Claim Settlement Take?

The claim settlement timeline in India varies:

- Cashless claims → usually a few days

- Reimbursement claims → 7–15 days after submission

Timelines depend on documentation and insurer efficiency.

Cashless vs Reimbursement Claims: Which Is Better?

When understanding the car insurance claim process in India, many people are confused about whether to choose cashless or reimbursement claims.

Cashless Claims (Recommended)

Cashless claims are generally preferred because:

- No upfront payment required (except deductions)

- Faster processing

- Less paperwork

Best for: emergency situations and major repairs

Reimbursement Claims

Reimbursement claims are useful when:

- You prefer a specific garage not in the network

- Network garages are unavailable

However:

- You must pay the full amount first

- More documentation is required

- Processing time is longer

For most car owners, cashless claims are more convenient in the car insurance claim process in India.

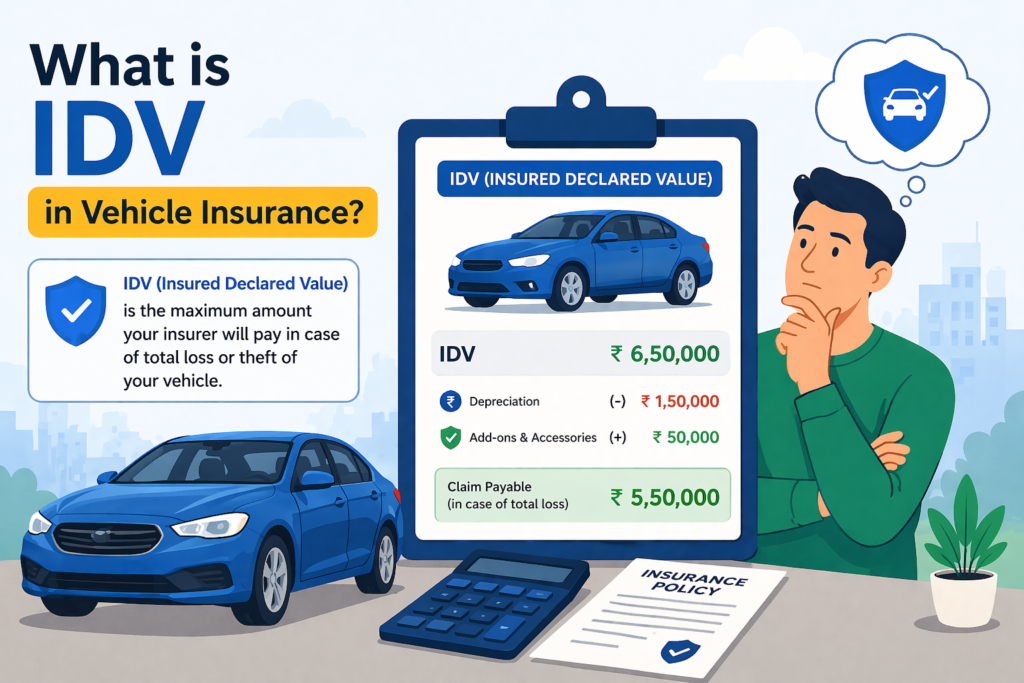

Role of IDV in Claim Settlement

Your Insured Declared Value (IDV) plays a major role in the car insurance claim process in India.

IDV represents the current market value of your car.

It determines:

- Maximum claim amount

- Compensation in case of total loss or theft

If your IDV is too low:

- You receive less compensation

If it’s too high:

- You pay higher premium unnecessarily

Also read: What Is No Claim Bonus (NCB) in Car Insurance?

Impact of No Claim Bonus (NCB)

Another important factor in the car insurance claim process in India is the No Claim Bonus (NCB).

If you make a claim:

- Your NCB is reduced or reset

- Your next premium increases

That’s why:

For small damages, it may be better to:

- Pay out of pocket

- Keep your NCB intact

What Happens in Case of Total Loss?

In case your car is completely damaged or stolen:

- The insurer pays the IDV amount

- Deductibles are applied

- Policy is terminated after settlement

This is called a total loss claim

Understanding this part of the car insurance claim process in India is crucial for major incidents.

Add-ons That Improve Claim Experience

Certain add-ons can make the car insurance claim process in India smoother:

1. Zero Depreciation Cover

- No deduction on parts

- Higher claim payout

You can read: Zero Depreciation Car Insurance Explained

2. Engine Protection Cover

- Covers engine damage due to water ingress

- Important during monsoons

3. Roadside Assistance

- Helps during breakdowns

- Provides towing and emergency support

When Can a Claim Be Rejected?

Understanding claim rejection reasons is important in the car insurance claim process in India.

Claims may be rejected if:

- Driver does not have a valid license

- Policy has expired

- Drunk driving is involved

- Damage is outside policy coverage

- Delay in informing insurer

Always follow policy terms carefully.

Final Tips for First-Time Claimants

If this is your first time dealing with the car insurance claim process in India, keep these tips in mind:

- Stay calm and document everything

- Take photos of the damage immediately

- Contact your insurer before taking action

- Keep copies of all documents

Being prepared can make the entire process faster and stress-free.

Tips for a Smooth Claim Process

To make the car insurance claim process in India easier:

- Always keep policy details handy

- Choose insurers with strong claim records

- Use network garages when possible

- Understand your coverage (IDV, NCB, add-ons)

Final Thoughts

The car insurance claim process in India may seem complicated at first, but it becomes simple when you understand each step. By informing your insurer on time, submitting the right documents, and following the correct process, you can ensure a hassle-free experience.

Being prepared and informed is the best way to handle unexpected situations and get the most out of your insurance policy.

Also read: What Is IDV in Vehicle Insurance?

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Insurance products are complex; please consult with a certified advisor before making a final decision.