Car insurance remains legally important in India regardless of how old a vehicle becomes. Many owners of older cars often look for ways to reduce insurance costs because the market value of the vehicle decreases over time. While lowering premiums is possible, choosing the right coverage is equally important to avoid financial risks during accidents, theft, or third-party liabilities.

For old cars, insurance premiums are usually lower compared to new vehicles because the Insured Declared Value (IDV) declines with age. However, selecting the cheapest policy without understanding coverage limits can create problems during claims.

In India, third-party car insurance is mandatory under the Motor Vehicles Act. Owners may additionally choose comprehensive insurance or standalone own-damage policies depending on the condition and value of the vehicle.

This article explains how low premium car insurance works for old cars in India, factors affecting premium costs, available policy types, methods to reduce premiums legally, and practical tips for selecting affordable insurance coverage.

What is Considered an Old Car in India?

Insurance companies generally classify vehicles older than 5 years as old cars for premium calculation and depreciation purposes. Cars above 10–15 years may require inspections during renewal, especially for comprehensive policies.

The value of a car reduces every year due to depreciation, which directly impacts insurance premiums.

Best Add-On Covers for Bike Insurance in India (2026 Guide)

Typical Car Age Categories

| Vehicle Age | General Insurance Impact |

|---|---|

| 0–5 years | Higher IDV and higher premium |

| 5–10 years | Moderate IDV and reduced premium |

| Above 10 years | Lower IDV and lower own-damage premium |

| Above 15 years | Limited comprehensive options in some cases |

Why Insurance Premiums Reduce for Old Cars

Insurance premiums for old vehicles are usually lower because insurers consider several depreciation-related factors.

Main Reasons for Lower Premiums

| Factor | Effect on Premium |

|---|---|

| Reduced market value | Lowers own-damage premium |

| Lower IDV | Reduces insurer liability |

| Fewer repair payouts | Smaller claim settlements |

| Lower replacement cost | Lower compensation amount |

However, third-party premiums are regulated differently and may not reduce proportionally with vehicle age.

IRDAI regulates motor third-party insurance frameworks in India.

Types of Car Insurance Available for Old Cars

1. Third-Party Car Insurance

Third-party insurance is the minimum legal requirement in India.

It covers:

- Injury or death of third parties

- Third-party property damage

- Legal liabilities arising from accidents

It does not cover damage to the insured vehicle.

According to Indian regulations, third-party insurance is mandatory for all vehicles operating on public roads.

Features of Third-Party Insurance

| Feature | Details |

|---|---|

| Legal Requirement | Mandatory |

| Covers Own Car Damage | No |

| Premium Cost | Lower |

| Suitable For | Very old cars with low market value |

2. Comprehensive Car Insurance

Comprehensive insurance covers:

- Third-party liabilities

- Damage to own vehicle

- Theft

- Natural disasters

- Fire damage

This type of policy is more expensive than third-party insurance but offers broader protection.

Features of Comprehensive Insurance

| Feature | Details |

|---|---|

| Third-party cover | Included |

| Own damage cover | Included |

| Theft protection | Included |

| Natural disaster cover | Included |

| Premium | Higher than third-party |

3. Standalone Own-Damage Insurance

Standalone own-damage insurance covers damages to the insured vehicle but excludes third-party liabilities.

This policy must be paired with active third-party insurance.

IRDAI allowed insurers to offer standalone own-damage motor insurance policies after regulatory changes.

How to Renew Expired Bike Insurance Online

Which Insurance is Best for Old Cars?

The ideal insurance type depends on:

- Vehicle condition

- Resale value

- Usage frequency

- Repair costs

- City risk exposure

Insurance Recommendation Based on Car Age

| Car Condition | Recommended Policy |

|---|---|

| Good condition, regular use | Comprehensive policy |

| Low-value car, limited use | Third-party policy |

| Moderately old but well-maintained | Comprehensive with fewer add-ons |

| Rarely used old car | Basic third-party cover |

Consumables Cover in Car Insurance?

How to Get Low Premium Car Insurance for Old Cars

1. Opt for Third-Party Insurance if Appropriate

For vehicles with very low market value, many owners choose only third-party insurance because repair costs may exceed the car’s worth.

Third-party insurance is generally the cheapest legal option available.

However, it does not protect your own vehicle against accident damage or theft.

2. Reduce Unnecessary Add-Ons

Add-ons increase premiums significantly.

For old cars, some add-ons may not provide meaningful value.

Common Add-Ons That Increase Premiums

| Add-On | Usually Needed for Old Cars? |

|---|---|

| Zero depreciation | Often costly for old cars |

| Engine protection | Depends on vehicle condition |

| Roadside assistance | Useful in some cases |

| Consumables cover | Optional |

| Return-to-invoice | Usually unavailable for older vehicles |

3. Maintain a No Claim Bonus (NCB)

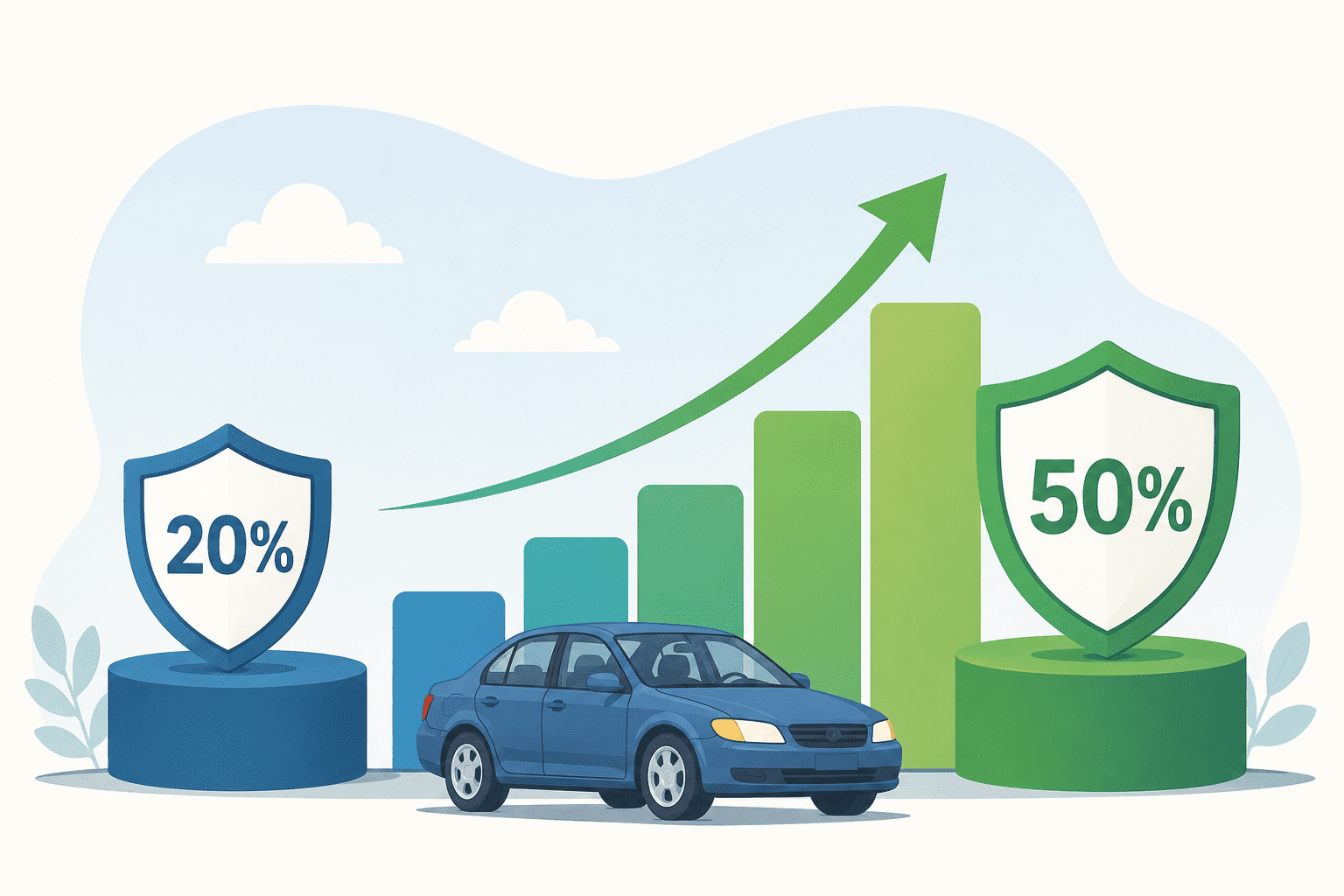

No Claim Bonus is one of the most effective ways to reduce insurance premiums.

NCB is a discount provided for claim-free years.

What Is No Claim Bonus (NCB) in Car Insurance and How It Works?

According to multiple insurers and insurance industry references:

- NCB starts at 20% after one claim-free year

- It can increase up to 50% after consecutive claim-free renewals (https://www.bajajfinserv.in)

Typical NCB Structure

| Claim-Free Years | NCB Discount |

|---|---|

| 1 year | 20% |

| 2 years | 25% |

| 3 years | 35% |

| 4 years | 45% |

| 5 years or more | 50% |

NCB applies only to the own-damage premium portion and not to third-party premiums.

Important Factors Affecting Premiums for Old Cars

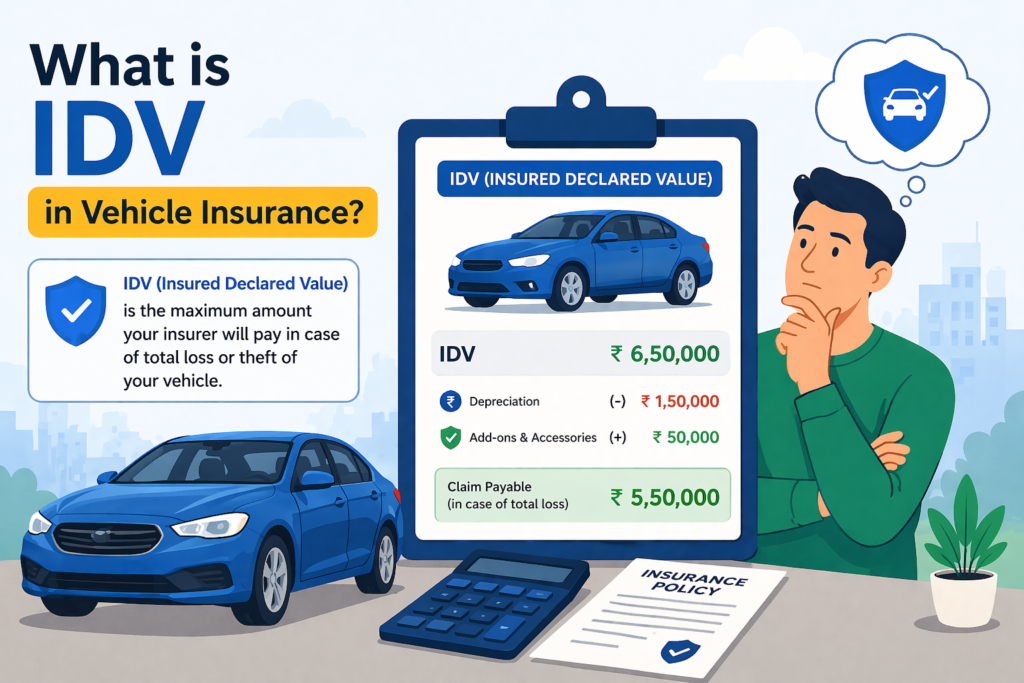

1. Insured Declared Value (IDV)

IDV is the approximate current market value of the car.

Lower IDV means:

- Lower premium

- Lower claim payout

Choosing an unrealistically low IDV may reduce claim compensation.

What is IDV in Vehicle Insurance? How to Calculate the Right Value for Your Car 2026

2. City of Registration

Premiums are often higher in metro cities because:

- Accident rates are higher

- Theft risks are greater

- Repair costs are expensive

3. Claim History

Frequent claims can increase future premiums and reduce NCB eligibility.

4. Vehicle Usage

Cars used occasionally may attract lower risk assessments compared to heavily used vehicles.

Should You Buy Comprehensive Insurance for an Old Car?

This depends on the vehicle’s condition and market value.

Comprehensive Insurance May Be Useful If:

- The car is well-maintained

- Repair costs are high

- The vehicle is parked outdoors

- The car is frequently driven

- Spare parts remain expensive

Third-Party Insurance May Be Enough If:

- The car has very low resale value

- Repairs are inexpensive

- Usage is minimal

- The owner can bear repair expenses personally

Indian law still requires at least third-party insurance for all vehicles.

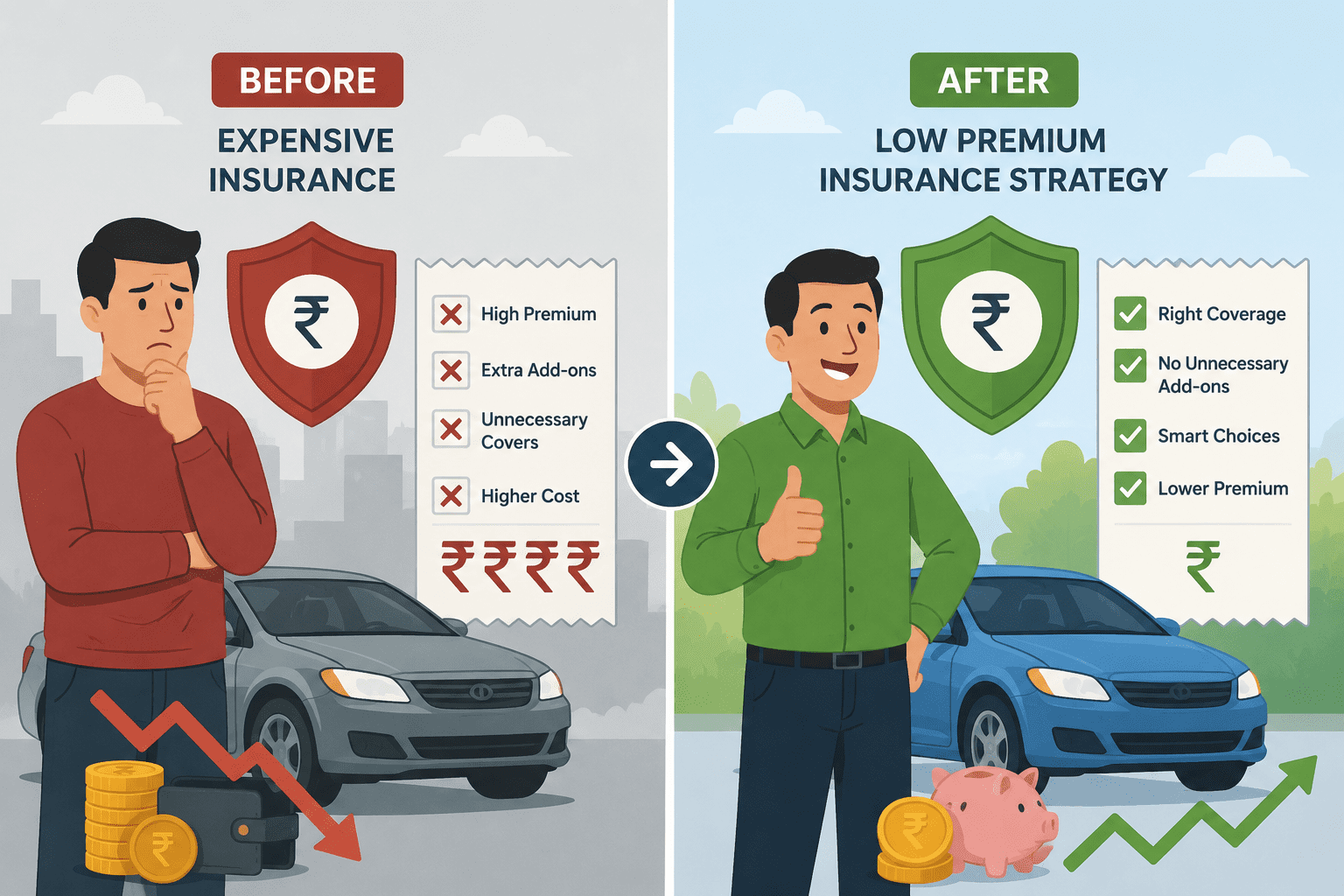

Common Mistakes to Avoid While Buying Cheap Insurance

1. Choosing Only Based on Lowest Price

Very cheap policies may:

- Have limited support

- Exclude useful coverage

- Include high deductibles

2. Hiding Previous Claims

Providing false information about NCB or claim history can lead to claim rejection.

A consumer dispute case highlighted that incorrect NCB declarations can invalidate claim eligibility.

3. Letting the Policy Lapse

If the insurance policy lapses for an extended period:

- NCB benefits may expire

- Vehicle inspection may become mandatory

- Renewal costs may increase

Insurance sources mention that NCB can lapse if renewal is delayed beyond permitted timelines.

Benefits of Buying Car Insurance Online for Old Cars

Online insurance renewal has become common in India.

Key Advantages

| Benefit | Explanation |

|---|---|

| Faster comparison | Multiple insurers can be compared |

| Lower premiums | Reduced intermediary costs |

| Easy renewal | Digital process |

| Instant policy issuance | Faster documentation |

| Access to discounts | Online offers may apply |

Tips to Lower Car Insurance Premiums Legally

Practical Ways to Save Money

| Method | Potential Benefit |

|---|---|

| Retain NCB | Significant discount |

| Avoid unnecessary claims | Preserves bonus |

| Remove unused add-ons | Lowers premium |

| Compare policies online | Better pricing |

| Choose higher deductibles carefully | Reduces premium |

Is Zero Depreciation Cover Useful for Old Cars?

Zero depreciation cover is generally more beneficial for newer vehicles because insurers pay full replacement cost without depreciation deductions.

For old cars:

- Premiums may become expensive

- Some insurers may not offer it

- Claim benefits may be limited relative to vehicle value

Owners should compare the extra premium against the actual market value of the car.

Final Thoughts

Low premium car insurance for old cars in India is achievable when vehicle owners choose coverage based on the actual value and usage of the vehicle. Third-party insurance remains the cheapest legal option, while comprehensive insurance may still be worthwhile for well-maintained older cars.

Maintaining a No Claim Bonus, avoiding unnecessary add-ons, renewing policies on time, and comparing online insurance options can significantly reduce premium costs without violating legal requirements.

Car owners should avoid selecting policies solely on price and instead focus on adequate protection, claim support, and policy transparency. Even older vehicles can create substantial financial liability during accidents, making proper insurance coverage important regardless of vehicle age.

Reference Links

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Insurance products are complex; please consult with a certified advisor before making a final decision.